Intelligent Income

Dear Client,

Thank you for entrusting Homestead Financial with your capital. Please read below for an update on our firm and investment strategy. You can read prior newsletters at https://homesteadfp.com/category/newsletter/

Investment strategy

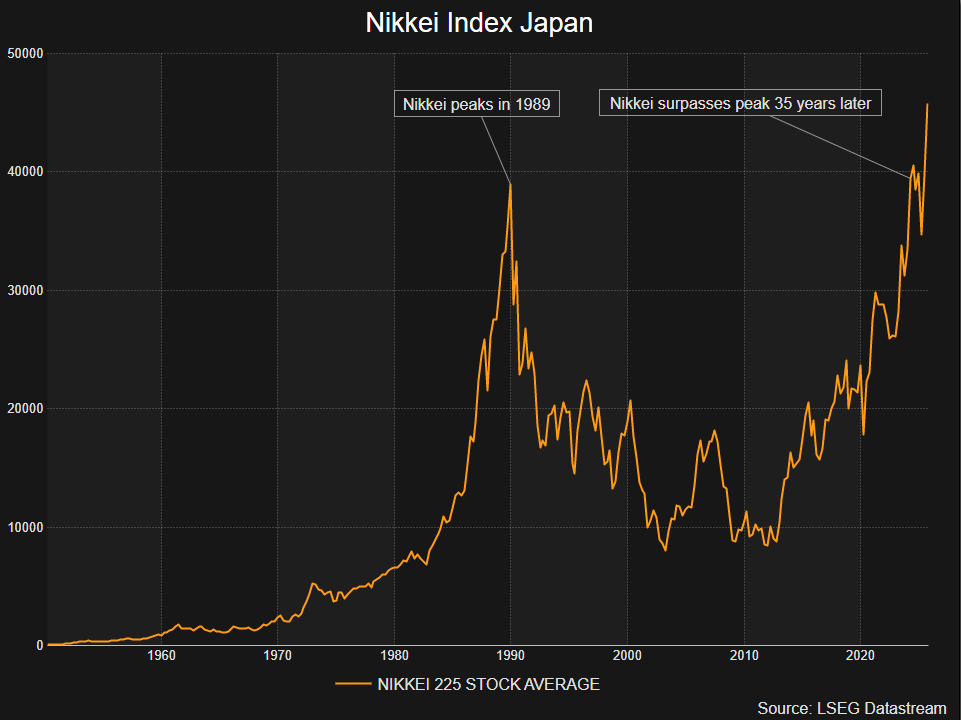

When Japan’s stock market peaked in 1989, it came as a surprise to many. Investors at the time had been conditioned to believe—indeed, EXPECT—that the Nikkei would appreciate indefinitely year after year. Why would anyone expect otherwise? After all, it had gone up for almost two decades! For the better part of a generation, anyone who questioned the rally or stood in its way was proven incompetent or inept by the Nikkei’s inexorable rise. Understanding the psychology of a bubble is crucial for investors, particularly in the current environment which, as we’ll discuss in a moment, has some markings of a bubble. But first, step back in time to 1989 and consider what Japanese citizens witnessed:

- The Nikkei stock market average traded at 60x earnings (an earnings yield of 1.6%) with extreme concentration among its constituents.

- The value of one company, Nippon Telegraph & Telephone, eclipsed the entire GDP of Germany.

- Taxi drivers and salarymen increasingly played the role of speculators, trading during lunch breaks. Golf course memberships changed hands for $3 million a piece.

- The land under the Imperial Palace in Japan was worth more than California

- Financial engineering (“zaitech”) became more prominent in the corporate sector

- Banks lent freely on inflated collateral values, not on cash flow

- Companies increasingly used their balance sheets to speculate on stock and property

The Japanese stock market crashed in 1990 and “lost decades” ensued, a thirty-year period during which asset prices deflated. A decade later, when the US experienced its own bubble in technology stocks, Japanese stocks remained under water. Japanese equities took 35 years to finally reclaim their 1989 peak in 2024.

The story of Japan is important because it illustrates the extremes faced by investors. Markets can diverge from reality for a very long time, so long that participants begin to embrace new narratives that justify what they observe. Those who resist this temptation and choose to deviate end up losing capital and influence over valuations. In this way, bubbles become self-fulfilling—as they inflate, they reward risk-taking and ever higher valuations while punishing independent thought and conservatism. This virtuous cycle continues…until it doesn’t.

Now consider the parallels between Japan in the 1980’s and the US today (particularly the technology sector):

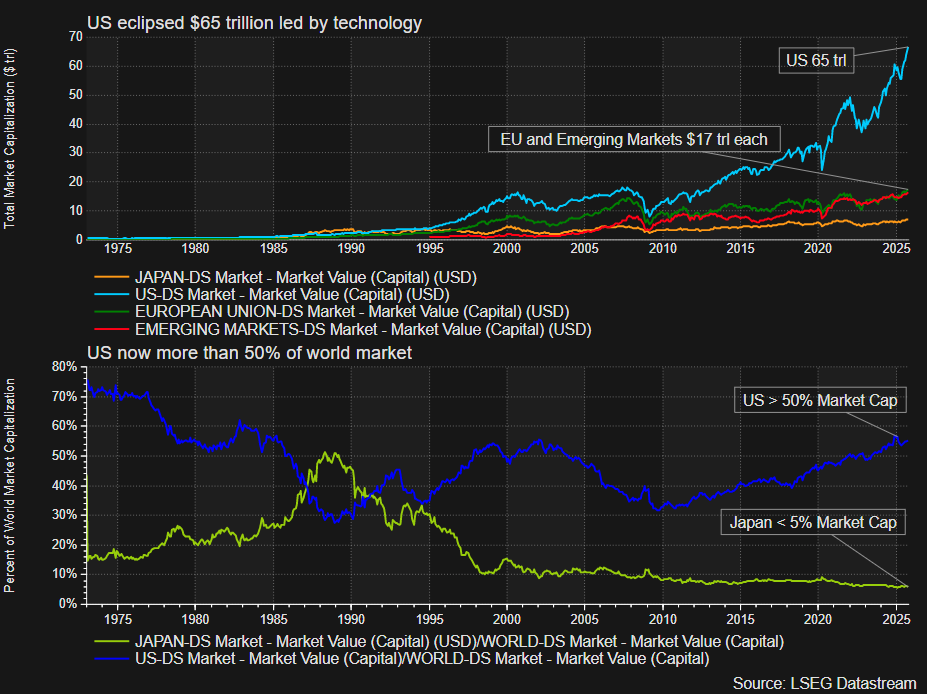

- The US share of global market capitalization has eclipsed 50%, a level last seen since 2000 for US and 1988 for Japan

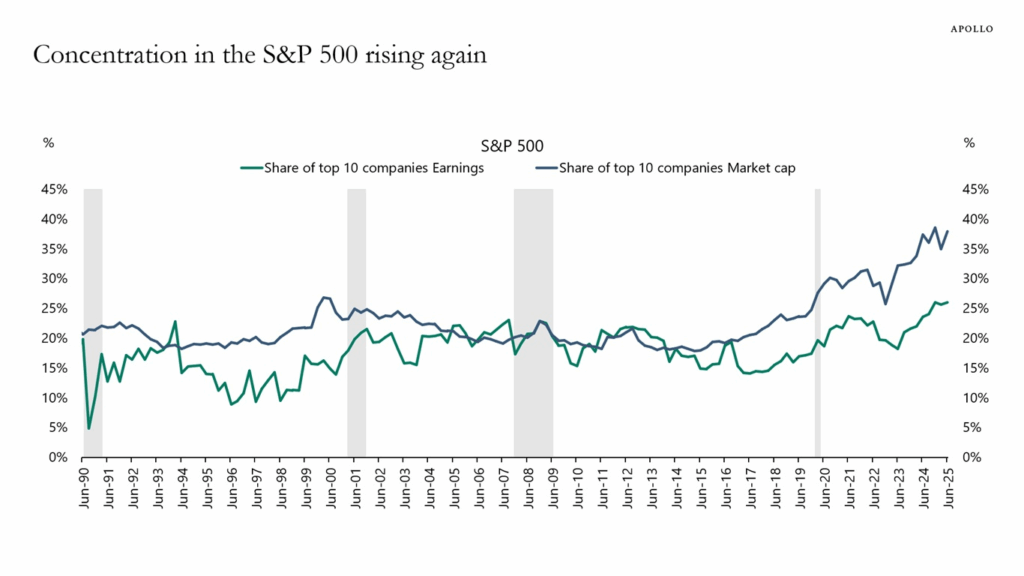

- Market concentration in the S&P has reached a 50 year high, with the top 10 companies representing 40% of total market capitalization. The top 8 companies, all technology, trade for an average price to earnings multiple of 50x.

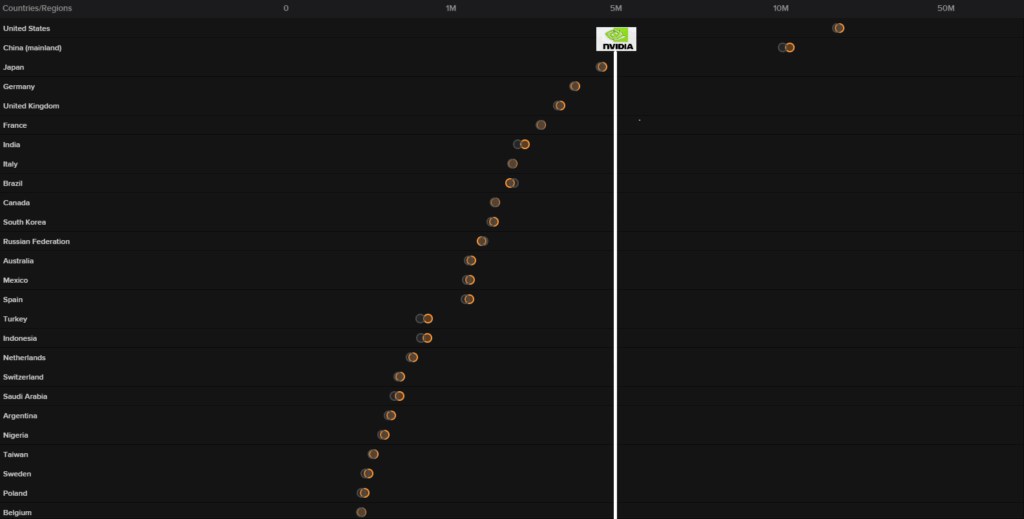

- Nvidia is now worth more than $5 trillion, larger than the GDP of every country except for China and the US

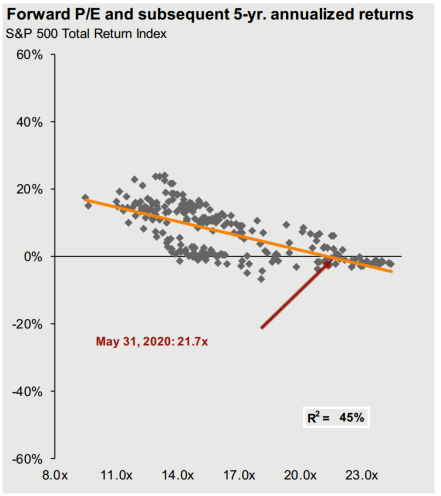

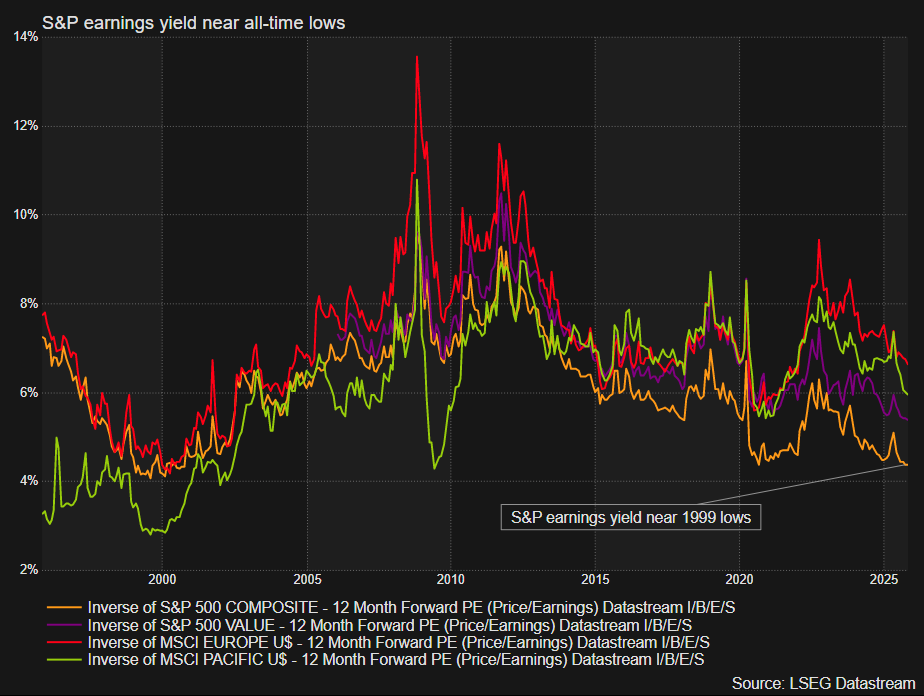

- The S&P trades with a forward earnings yield near 4%, approaching its all time low in 1999. This compares with 6-7% for Europe and Japan and a long-term average closer to 7%. Earnings yield is the inverse of price-to-earnings, which trades two standard deviations above its 40-year average.

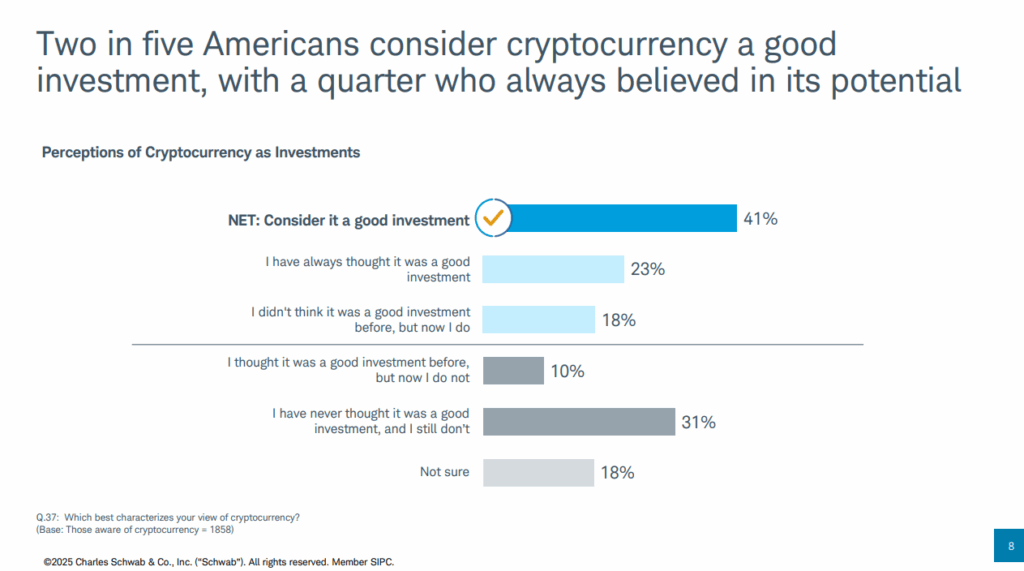

- Crypto is considered a good investment by 41% of Americans and makes up 10% of allocations

- Lending standards have fallen, fueling rampant growth in private credit, which now exceeds $2 trillion

- Capital spending on AI is projected to exceed 3 trillion through 2029, around what the US invests in housing

Like Japan in the late 1980’s and the US in the late 1990’s, the market is clearly exhibiting excessive levels of concentration, overvaluation, and speculation. This is why it made perfect sense last Friday when Berkshire Hathaway disclosed that their cash pile reached an all-time high of 380B in the third quarter of this year.

Staying the course

Homestead likes to make money, and we REALLY hate losing it. Given these overarching objectives, we remain disciplined on valuation and risk across our portfolios. This means focusing on cheap companies with good fundamentals and, where appropriate, holding some bond allocations (investment grade). While this approach may not “feel” good in the moment as we lag certain benchmarks, the upshot is that 1) a conservative posture provides insurance against excessive risk-taking and 2) cheap valuations increase the prospects for future returns.

{kind=link}

Homestead’s equity income strategy ended the quarter with a return of 4.9%, bringing its year-to-date return to 6.8%. We see plenty of value outside rich pockets in mega-caps and technology/communication. The earnings yield for our entire portfolio is over 8%, a solid figure by historical standards and roughly half the price of the S&P (4%). Particular areas of focus include industrials/cyclicals, building products, financials, and consumer staples all of which have lagged the eyewatering returns in the technology sector. This quarter we added Gildan Activewear, Inc. (GIL) to our holdings in the consumer discretionary sector after the company announced plans to acquire its competitor, Hanesbrands, for 2.2B in cash and stock. We have long admired Gildan’s management team and are excited about the potential earnings power for the combined business, which will span the market for basics and custom/printed apparel and will leverage Gildan’s production and go-to-market capabilities. On a pro-forma basis, we expect the business to earn between $5-6 of free cash flow, offering investors a multiple of around 10x today’s trading price while paying a dividend of between 1-2%. Gildan is a good example of a company outside of the technology sector, domiciled in another country (Canada, not in US indices or ETFs), that offers a compelling return with a double-digit free cash flow yield + growth.

Homestead continues to maintain a firm stance on risk, stepping into opportunities like Gildan as they present themselves while holding the line on valuation. The lopsided US market may be overvalued as a whole, but that does not necessarily hold true for individual companies that have been left out of the melt-up. Rest assured that we will stay the course, executing our strategy to hold good companies at good prices with a strong bias towards capital preservation. Thank you again for your support and don’t hesitate to reach out anytime.

Sincerely,

Supplemental Charts

japan’s nikkei stock market average

us market capitalization

s&p market concenration

s&p earnings yield (inverse of pe)

s&p forward price to earnings ratio

schwab crypto survey

nvda $5 trillion market cap exceeds GDP of most countries