Intelligent Income

Dear Client,

Thank you for entrusting Homestead Financial with your capital. Please read below for an update on our firm and investment strategy. You can read prior newsletters at https://homesteadfp.com/category/newsletter/

Investment strategy

In our Q4 2024 newsletter, we explored the relationship between politics and markets, concluding that markets typically discount political noise—except when earnings are directly affected. As political drama continued through early 2025, investors remained sanguine, embracing the narrative around deregulation and pro-growth policy and pushing equity indices to all time highs in February. On our view, the flurry of executive orders, rhetoric around tariffs, and rumblings from DOGE seemed to favor caution, so Homestead maintained a disciplined risk posture through 1Q25. When volatility spiked after Liberation Day in April, our equity allocation performed as expected with a drawdown of -9.6% against -12% for the S&P 500. As credit spreads widened and long-term interest rates increased, our short dated investment grade bonds provided ballast. After about a month, the S&P had fully recovered on the so-called TACO trade (Trump Always Chickens Out) as investors rushed back into risk assets. Looking back at this period of volatility, we can reflect on a few takeaways:

- Politics and markets: It reminded us that politics CAN bleed into markets IF they impact fundamentals. Trump’s tariffs on Liberation Day were a very real (even if unquantified) risk to earnings, which explains why the market reacted so violently.

- Proactive research: It highlights the importance of researching issues PROACTIVELY, as we did with tariffs in 4Q24 following Trump’s rhetoric on the campaign trail. Doing so reduces the need to scramble and make adjustments REACTIVELY during periods of market volatility.

- Signal vs noise: There is a difference between ACTIONABLE information and NOISE. Comments on social media or rumors in the press should drive investment decisions only insofar as they have a real impact on companies.

- Balancing risk: Lastly it reminds us to consider both downside as well as upside in our approach to capital allocation, within equities and across asset classes. Discipline is paramount as we navigate a period of social, political, and economic transition against a backdrop of high valuations.

the gordian knot of Trade, currency, and interest rates

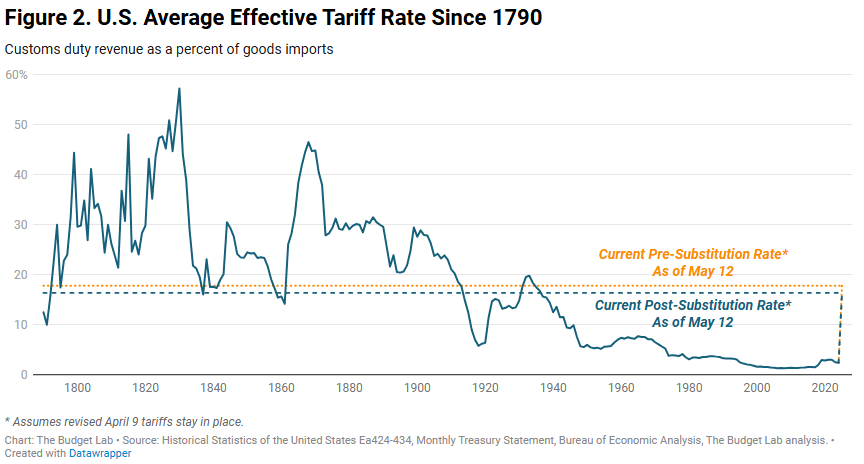

Trade deserves some discussion given its prominence in the headlines and potential to impact markets and the economy. Tariffs have been a feature of American policy since the founding of the country. The 19th century saw very high tariffs, peaking with the 1828 “Tariff of Abominations,” which triggered Southern resistance. Tariffs stayed high through the Civil War to support Northern industry. The frequently cited Smoot-Hawley Tariffs of 1930 raised duties during the Great Depression, leading to global retaliation and contributing to the Great Depression. After World War II, the United States sought to remove trade barriers and promote free trade through GATT (1947) and later the WTO (1995). This together with the role of the dollar as reserve currency allowed the US to run large trade deficits as it has done since the 1970s. The bottom line is that trade has seen different regimes each spanning decades, shifts in policy can last a while, and proposed tariff rates around 20% are the highest in a generation.

Normally, a country running a large trade deficit would see their currency weaken as they print money to pay for goods and services. However, because we are the reserve currency, our trading partners choose to park their IOUs in treasury bonds and other financial assets in the United States. This props up the value of dollar relative to other currencies and helps to lower interest rates on our debts. It’s good for US consumers and our indebted government but makes life harder for our manufacturers and exporters.

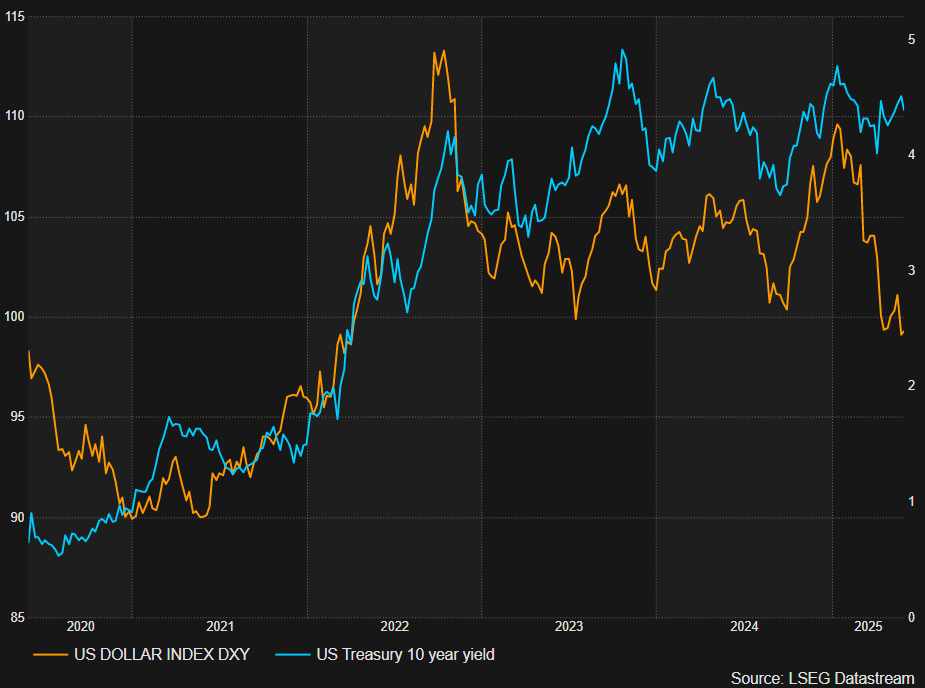

Trump wants to counteract these forces using tariffs, but as we’ve seen tariffs can be difficult to implement given the complexity of global supply chains. Another way to achieve a similar result would be to devalue the dollar, making it easier for our domestic producers to compete in foreign markets and harder for consumers to buy cheap foreign goods. In addition to helping trade, a weaker dollar would also reduce our large national debts in dollar terms. A recent precedent for this would be the Plaza Accord of 1985, where the G5 countries agreed to adjust their currencies relative to the dollar to offset the impact of high interest rates. There are signs that such a shift may already be underway, with the US Dollar falling more than 10% year-to-date as Trump pressures the federal reserve to lower short term interest rates. As US investors, we should consider the ramifications:

- Lower short term rates and a weaker dollar are inflationary, supporting higher long-term interest rates. Higher rates tend to cheapen financial assets and make financing harder to come by. This can impact companies that rely heavily on debt and assets with long duration (low cash yield).

- A weaker dollar could benefit US companies with domestic production and access to export markets. Ironically, some of these companies may appear, at the moment, to be victims of the current trade war.

- A weaker dollar also improves the returns on assets denominated in foreign currencies. Foreign equities are relatively cheap to begin with and would be even more attractive in the context of a weakening dollar.

- Tariffs and other forms of protectionism may remain a feature of US policy for some time, even if the ultimate outcome looks different from Trump’s proposed levies. History suggests these regimes can continue for some time as imbalances persist.

Within the portfolio, we made a number of adjustments in recent months as we assessed risks and opportunities following Q1 earnings season and recent actions from the Trump administration. In our view, the pharmaceutical industry stood out as being on the wrong side of several emerging trends: government initiatives to negotiate prices (bipartisan and global), changing criteria around drug approvals, revisions to public guidance on the use of medication, and tariffs all represent headwinds. While optically cheap, we decided to sell our positions in Merck and Pfizer (both pureplay pharmaceutical companies) and allocate to other cheap opportunities with better prospects. We retained Johnson & Johnson given its strong balance sheet, smaller patent cliff, and balance between drugs and medical devices. Proceeds from these sales, together with capital from the disposition of some of our more cyclical and fully priced holdings in mid-March were redeployed into Ally (bank), Westlake (building products), UnitedHealth (managed care), and Constellation Brands (beer). These adjustments added some cheap, high quality holdings to our portfolio while maintaining an earnings yield of 8%, forecasted dividend yield close to 3%, and weighted average beta below 75%. While evidence supports a soft landing and a return to growth in 2Q (no recession), we continue to favor a low risk profile given the relative affordability of low beta stocks and the still elevated risk of tail events like military conflict or economic dislocation.

firm update

Homestead continues to refine the tools and methods we use to drive our value-focused investment process. In idea generation, we’ve incorporated a new analytical model that uses scoring algorithms to highlight cheap securities within the universe of ~5200 publicly traded dividend paying securities on US exchanges. This model will complement and improve our fundamental, value-oriented screening process. For fundamental (company level) analysis, we’ve acquired access to an expert transcript library with over 100,000 interviews covering public and private companies across all sectors. These interviews, available in summarized and searchable formats through an AI-enabled platform, enrich our understanding of companies by shedding light on topics discussed outside of the quarterly earnings cycle. We also subscribed to a database of over 4000 company financial models, which are maintained by a team of more than 100 analysts. Lastly, we continue to embrace Schwab’s new portfolio management platform, which automates and streamlines the process of trading portfolios while adding capabilities like tax loss harvesting. These new tools and capabilities continue to advance the speed and accuracy of our processes with the ultimate goal of preserving and compounding our assets over time. Thank you again for your continued trust and support, and please reach out anytime to discuss investments, the firm, or anything else that’s on your mind.

Sincerely,

Supplemental Charts

US tariffs over time

US trade balance percent of gdp

us dollar vs 10 year bond yield

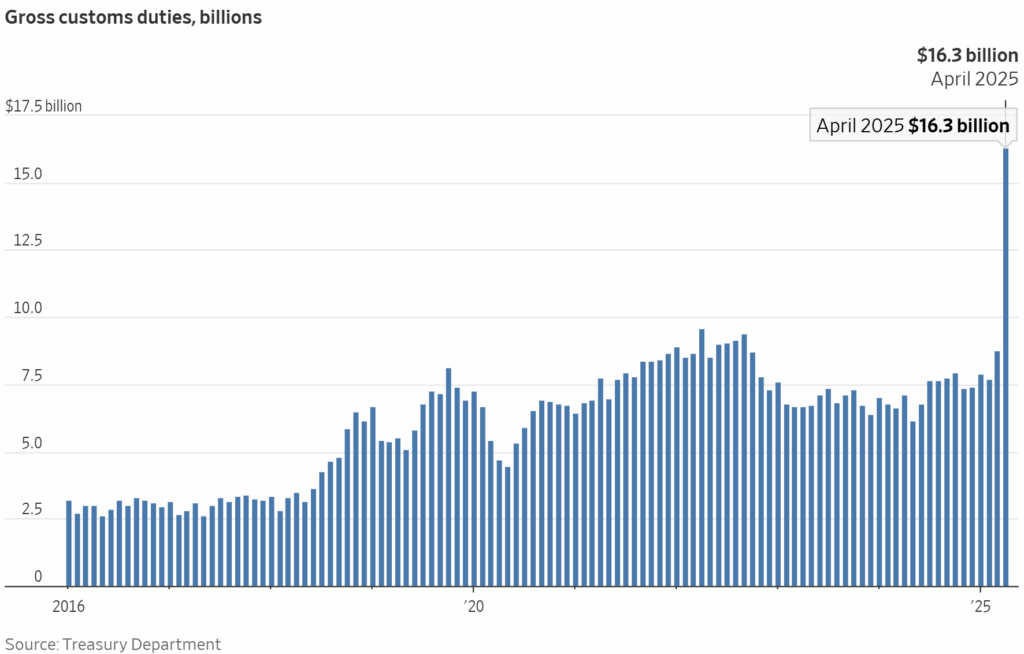

US tariff collection