Intelligent Income

Dear Client,

Thank you for entrusting Homestead Financial with your capital. Please read below for an update on our firm and investment strategy. You can read prior newsletters at https://homesteadfp.com/category/newsletter/

investment strategy

The Homestead Income Portfolio ended first quarter 2026 up 3%, giving back some gains late in the quarter after a strong start to the year. Our performance in the first quarter exceeded the Russell 1000 Value index (+2%) and the S&P 500 (-4%) but lagged dividend peers (+5%) as we remain underweight companies exposed to the AI capex cycle and have very little exposure to energy. For a more granular detail on adjustments to the portfolio and allocation please see our slide deck using the link in your client email.

Now that we have dispensed with the formalities, let’s get down to the brass tacks on two issues driving markets now: 1) the AI cycle (yes…it is a cycle) and 2) the war in Iran, oil, and inflation.

ai everywhere

Ok, so for starters, I did not write this newsletter with AI and will not use AI to write letters in the future. That would be disingenuous. This letter is a communication directly from me to you. Having said that, I do ask Claude to check my grammar and facts, and I can report that it rarely finds any meaningful revisions, so chalk one up for the humans!

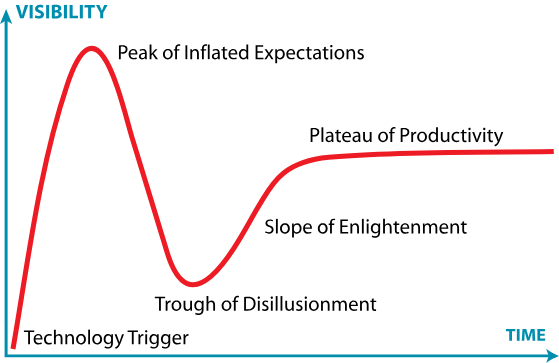

AI is an amazing technology that we will all use to improve our lives and work for years to come. Like the internet (and other digital goods), it will become ubiquitous and available to everyone, and as this happens it will reshape the economy. As business people and individuals, we are in awe of its capabilities and see the need to harness its power to improve our processes. A software project that took an army of developers months to complete can now be achieved by someone with no coding experience, whether its migrating between systems or building an entirely new stack. The possibilities are endless, and very real. Welcome to the hype cycle…

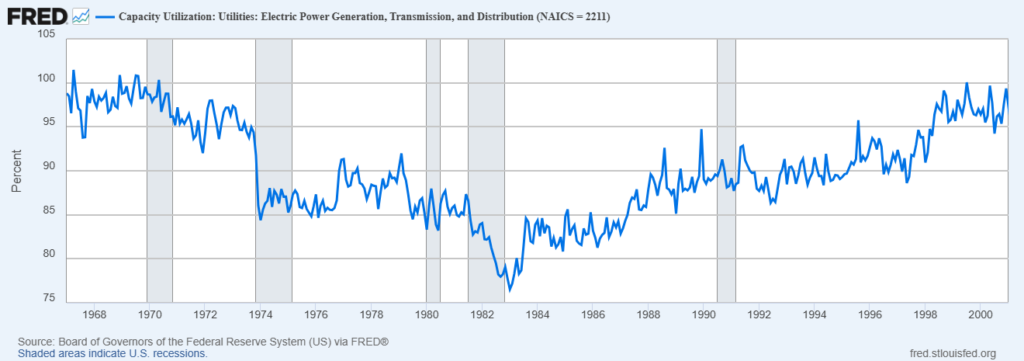

When the personal computer hit desks in the 1980s, inflation was running in the teens and interest rates were nearly as high…(sound familiar? give it some time…). Famed Economist Robert Solow remarked that he saw computers everywhere but in the statistics, and what he meant was that rapid adoption of computers didn’t seem to be affecting efficiency or output in any perceptible way (aside from higher electricity consumption)…and that lasted until the 90s when the computers combined to form “the internet” driving the hype cycle known as the dot com boom bubble. Looking back, we can see that the internet changed everything, driving productivity in the 90s and enabling new business models like social media and search, but this took time and many of the darlings in 1999 never made it to the trillion dollar club (Google, Microsoft, Meta, etc) or even survived the dot com bust. The current cycle has many parallels with the dot com bubble. Consider the following:

- AI is a digital technology that is replicable (list of llms)

- there is a physical element behind it (data centers), which is similar to fiber optic overinvestment in the 90s

- valuations are ballooning as investors extrapolate growth and assume “it’s different this time”

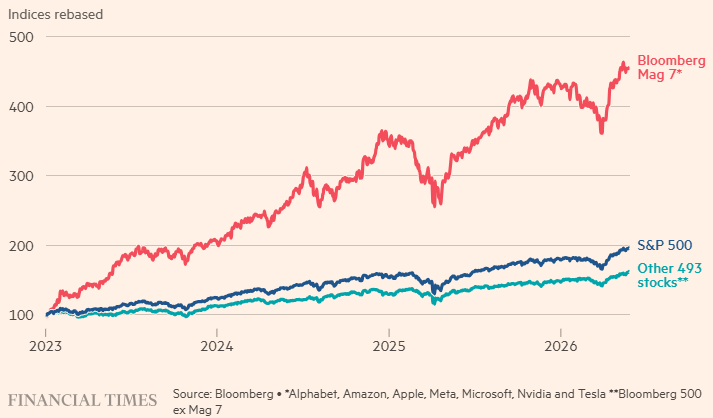

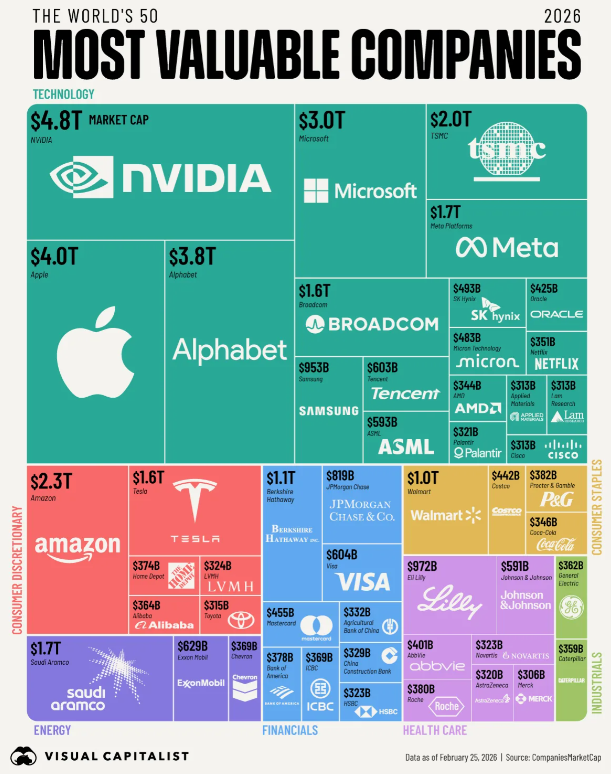

- the market has extreme concentration, focused on information technology

- the mere mention of AI adds billions of dollars to a company’s market capitalization

- AI companies continue to use circular financing, vendor financing, and debt to fund growth well in advance of cash flow

So now that we have established the internet/dot-com analog, lets think like a value investor about how this plays out, understanding that history tends to rhyme more than it repeats:

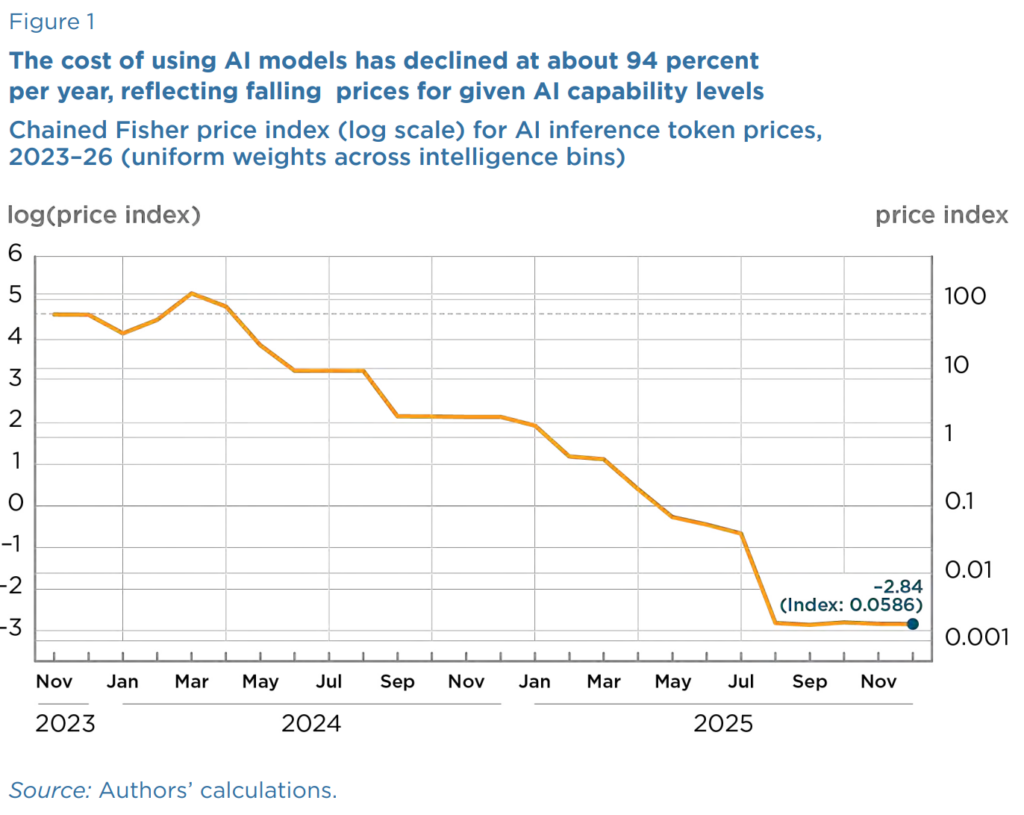

- once built, data centers and their hosted LLMs will become cheap and available, much like the internet (think ai for everyone). This is already happening with opensource and Chinese models (deepseek cuts pricing 75%).

- falling prices and overcapacity make it difficult for AI model providers meet revenue expectations

- investors realize the physical market for datacenters and hardware, now on a massive capex cycle, has been overbuilt

- AI moves to the trough of disillusionment before a smaller group of winners emerge from the rubble. These winners may not even include “first movers” like OpenAI

- broad availability of intelligence drastically reduces the cost of software development and migration. Software goes from an 80% gross margin business with high barriers to entry to ubiquitous and and almost free

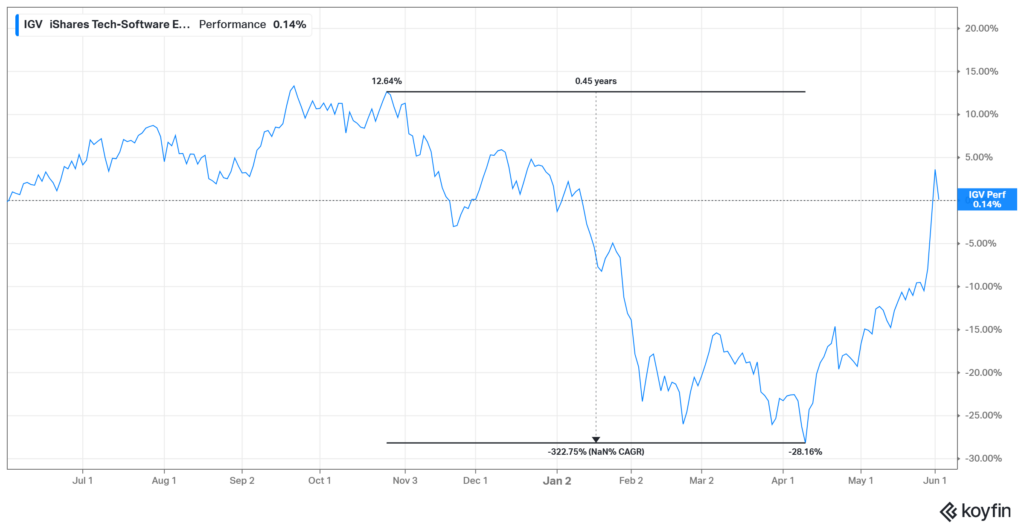

Through this lens, it makes perfect sense when software stocks swooned earlier this year. A little more perplexing are the stretched valuations in IT hardware, but as Ben Graham once said, the market is a voting machine in the short-term and a weighing machine in the long-term. Give it some time.

“claude, hand me a screwdriver”

Jensen Hwang, the CEO of NVidia, muses that we need more plumbers and electricians to build infrastructure for AI, and he is partially right. But it is not just IT infrastructure we need to build; we need supply chains to satisfy our demand, reinvigorate exports, and close our trade gaps. This process will take years and touch many end markets, ranging from foods to materials and manufactured goods. Furthermore, AI itself remains largely confined to shuffling bits and bytes (the virtual world) and can do very little to relieve constraints in the physical world (inflation). Because of this “barrier to entry”, the tangible businesses in our portfolio are shielded to some degree from the destructive gale of AI, and actually could benefit from the productivity it creates. As you look at our holdings, think about how each company will navigate the risks and opportunities posed by AI. Trains, planes, automobiles, materials, healthcare, clothing, packaging, etc. For most of our companies, AI is not a risk but an enabler. This is an important distinction given the disruptive potential of artificial intelligence.

As investors crowd into the AI trade and push valuations in tech and related sectors to new highs, they also leave behind a lot of good companies at bargain prices. We are focused intently on evaluating those opportunities, as they 1) insulate us from loss and 2) provide an attractive entry point. One example of an area where we see opportunity is housing and related industries. Many companies exposed to housing are sound business with good competitive moats in the midst of a multi-year slump tied to interest rates, inflation, and other factors. The same can be said for many consumer facing businesses, particularly those with sensitivity to interest rates (cars, appliances, recreational vehicles, etc.). When conditions normalize and consumer spending rebounds, these businesses could see significant upside. Berkshire agrees.

iran, oil, and inflation

A quick thought on oil, Iran, and inflation. Note to Trump: Iran is not Venezuela! The size, the location, the regime…The good news is that there are two types of oil shocks: short-term (think pandemic) and long-term investment-related (peak oil). The former can be solved without needing to FIND NEW OIL, while the latter is a long investment cycle that calls into question the adequacy of potential supply more broadly. We entered the Iran crisis oversupplied, with oil trading very close to its marginal cost, even as countries like Venezuela and Iran produced half their potential. Today the spot price is 2x that level and the futures curve is in backwardation (downward sloping) suggesting that prices should ease over time. Not only do I agree with backwardation, I also think higher prices today and the potential for debottlenecking Hormuz may translate into even lower prices in the future. In my view, high oil prices are probably transitory.

On the other hand, inflation is a different matter. As I discussed last year, trade policy, immigration reform/tight labor, and a weak dollar continue to push inflation structurally higher. The latest surge in oil prices only adds to this secular trend. It will be interesting to see how Warsh approaches this problem: Arthur Burns or Paul Volker? For our part, Homestead will continue to keep the reigns on duration and valuation across our portfolios, as these are the best antidotes for inflation.

firm update

As clients you see what is held in your portfolios but you do not always see the process behind the holdings. I want to take an opportunity to bring you up to speed on how AI is transforming process at Homestead. I have been using AI as a research tool for several years now: first chats in ChatGPT, then projects for individual stocks or industries, then Claude last fall. I’ve also used AlphaSense for years along with some other tools with AI offerings. In January of this year, I installed Claude Cowork the day it launched for Windows and was blown away by what I saw.

…HELLO WORLD…

Some friends from Carnegie Mellon quickly turned me on to an open source platform for AI models and I began using it to build agents and tools that are now performing equity research for me utilizing dozens of LLMs, sometimes while I sleep. The philosophy has not changed at all—good companies at cheap prices—but the way I discover, research, and monitor opportunities is rapidly evolving. Think fewer screens and dashboards, more data, and a bunch of agents trained on different skills creating a lot of new information I didn’t have before. It has been exhilarating, and there is so much more to do. If you are ever curious and want to learn more about what I’ve built, don’t hesitate to give me a call.

Sincerely,

Supplemental Charts

Gartner Hype cycle

electricity consumption in pc era

it concentration

software reset

ai model costs

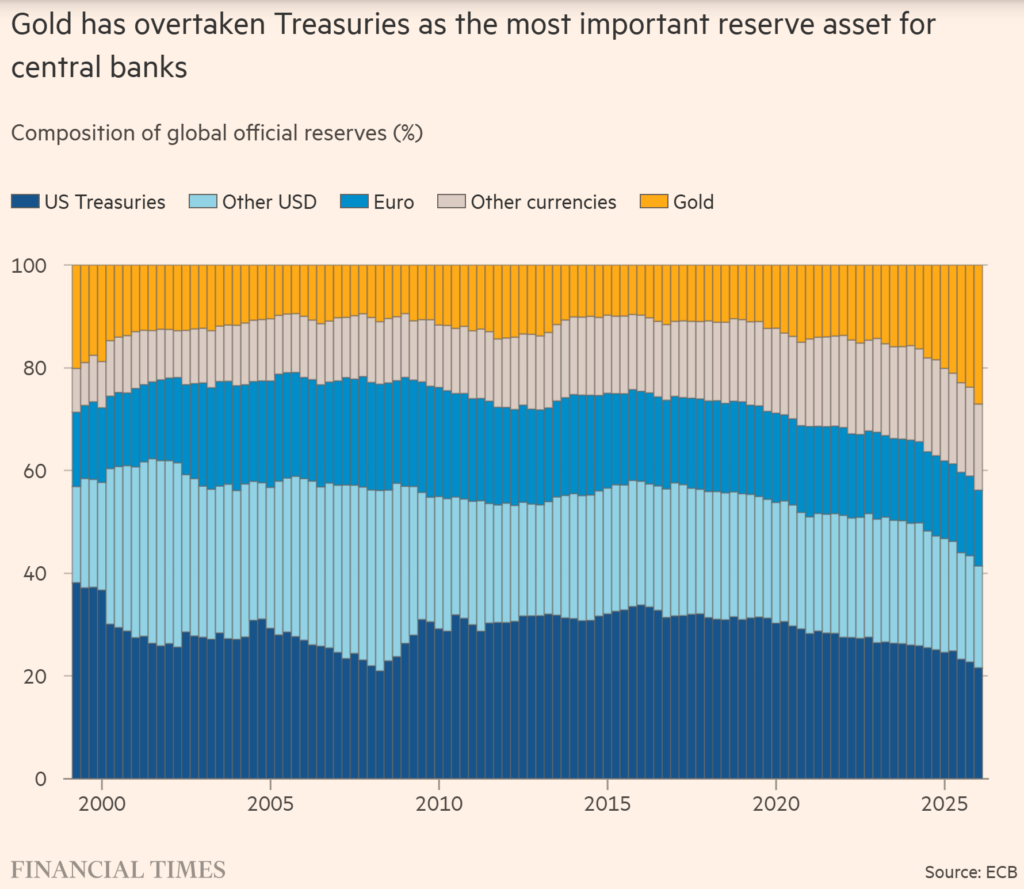

dedollarization